Home Insurance Discounts

(And how you can get started today)

Maggie Tiede is a writer and blogger based in Saint Paul, Minnesota. Maggie has worked as a freelance writer since 2013, when she began reporting on politics, local events, health, and human interest for the Grand Rapids Herald-Review.

Paul Martin is the Director of Education and Development for Myron Steves, one of the largest, most respected insurance wholesalers in the southern U.S.

Buying a house can be expensive, and the spending never stops there: Water heaters, septic tanks, flooded basements and more can all ruin your day at a moment’s notice. Luckily, home insurance doesn’t have to be another drain on your hard-earned cash, because discounts are out there.

And getting them could be as simple as a phone call. Our independent insurance agents can help you find the discounts you deserve, lower your bills, and get you back to the good things in life.

What Are Home Insurance Discounts?

When you insure your home, you're signing up to pay premiums (monthly, quarterly, or yearly payments that may be rolled into your mortgage) in exchange for coverage. If your home is damaged, your insurance company promises to pay as long as certain conditions are met.

Quite simply, home insurance discounts lower those premium payments. But insurance discounts don’t really work like the coupons you love. You don’t clip ‘em out of the Sunday paper and get free flood insurance with the purchase of two extra add-ons.

They’re more like a giant computer algorithm that the insurance company uses to calculate how likely your home is to get into trouble. The less likely damage or vandalism is, the less you’ll pay.

Things that might go into the formula include your age, gender, location, marital status, credit score and driving record. Two things that never go into the formula are your race and religion, since those characteristics are protected by law when it comes to insurance.

Another factor in home insurance discounts is the size of your deductible. A deductible is an amount of money for damage that you agree to pay before your insurance coverage kicks in.

The higher your deductible is, the lower your premiums will be, since the insurance company is on the hook for less money and they pass those savings on to you.

DID YOU KNOW?

It’s important to remember that not all discounts will be spelled out in your policy, even if they’re still saving you money.

You’ll probably know if you’re getting a military or veterans discount, but you might not realize you’re getting a marriage discount, too. It’s all part of the great algorithm.

Insurance companies (also called carriers) don't like to share their exact formulas with customers. It's key to their bottom line, so they consider it proprietary information. Luckily, we've got insider knowledge. Here's what carriers are really thinking when they offer you savings on your homeowners insurance.

Save on Home Insurance

Our independent agents shop around to find you the best coverage.

What Home Insurance Discounts Are Available?

The cost of your home insurance is mostly based on two things: the chance of your home getting damaged, and the potential cost to the insurance company if that damage does happen. Insurance payouts aren't tied to how much you paid for your home, they're based on how much your home will cost to rebuild.

Choosing a simple home that's cheap to build can discount your home insurance significantly.

The thing is, most people aren't going to shop for a home with nothing but insurance costs in mind. You want a home that looks nice, feels nice, and meets your needs. If that means having a whole mess of corners and recessed lights in every room, then so be it!

It pays to think about insurance costs before you buy a home, but it's probably never going to be a deciding factor. Luckily, there are other kinds of discounts you can score that aren't related to the replacement costs of your home.

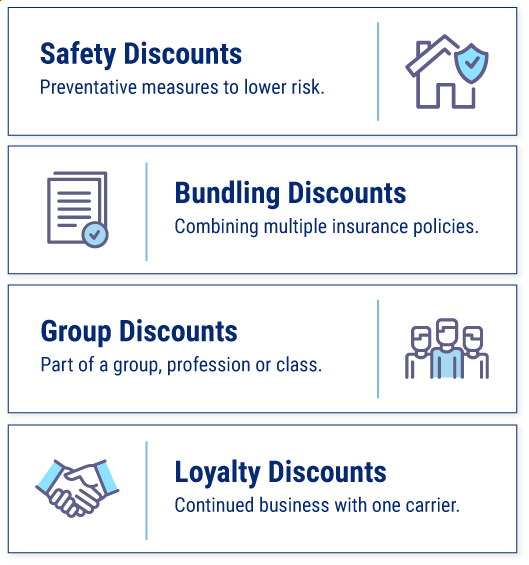

There are nearly as many home insurance discounts out there as there are insurance companies, but they can all be divided into four major types. And here they are:

4 Major Types of Discounts

- Safety discounts: These are given to those who take extra-special care of their home or have upgraded with special features that make it safer than average. Installing burglar alarms, sprinklers, or a high-quality roof are things that can get you safety discounts.

- Some safety discounts aren’t as obvious as others. In rural areas with spotty fire coverage, it’s possible to get a discount for having a pool. That’s because firefighters can use the water to put out a fire, saving your home. More on these in a minute.

- Bundling discounts: These are discounts you can get if you buy multiple types of insurance with the same company. Got a car? Great, because if you get both insured by the same company, they’ll probably cut you a deal. Ditto if you insure multiple homes with the same company.

- Group discounts: These are discounts you can get if you belong to a certain association or profession. Common group discounts include military discounts, teacher discounts, and government employee discounts. Other niche discounts include the ones for farmers, clergy, and even dentists.

- Loyalty discounts: These are self-explanatory: They reward customers who stay with the same insurance company for a long time. You might also get discounts for referring friends and family to your insurance company. So break out your Rolodex, it’s time to get that referral cash.

Each of those categories breaks down into a bunch of possible discounts you can qualify for. Here's a more exhaustive list of home insurance discounts:

- Sprinklers: Sprinklers put out fires faster, saving your life and your home. Discount!

- Fire extinguisher: If you keep one handy and know how to use it, this also nips fire damage in the bud. Another discount.

- Near a fire hydrant: The closer you are to a fire hydrant, the faster fires can be put out. Noticing a pattern? Fire is one of the biggest causes of home insurance claims. Insurance companies reward you for taking steps to lower that risk. Discount.

- Near a fire station: The less the distance between you and firefighters, the faster they can get you out of a fiery jam. Discount.

- Security system: Installing a security system helps keep thieves out and your belongings safe inside. Home insurance usually covers theft, so preventing theft nets you a discount. Get a security system that connects to your smoke alarms and you're really cooking with gas.

- New home: We learn new things all the time, like fire escapes are good and asbestos is bad. New homes take advantage of all this new knowledge, so they're usually safer. Discount.

- High-quality roof: Hail and wind damage are among the top reasons homeowners file a claim. A sturdy roof can lower your premiums. (Of course, it lowers your heating bill and looks nice, too. Sweet!)

- Tidy yard: When insurance reps visit your property, they like to see it looking spiffy. Neatly trimmed grass, shrubs, and trees lower fire risk and show the insurance company that you care about your property. Discount!

- Fresh paint: This goes along with the above. Fresh paint is safer and looks nicer. That's yet another discount for you.

- Pool/no pool: This one's weird. Normally, a pool is going to drive your insurance premiums up, since they can cause nasty injuries and they cost a lot to replace. The exception is if you live out in the boonies with no fire hydrants. Firefighters can use pool water to put out a fire, so insurance companies offer you a discount. Talk about an edge case.

- No trampoline: Trampolines are fun, amazing, awesome, terrible no good broken-arm factories. It's true. Your homeowners insurance might drop you altogether if you get a trampoline, and if they do cover you, they'll charge through the nose. No trampoline, big discount.

- Bundling: Carriers want your business, so they'll give you a discount on your home insurance if you add a car, motorcycle, life, or similar insurance policy with them. This is probably the easiest and most transparent insurance discount to get.

- Multiple homes: This is another type of bundling discount. If you own multiple homes, be sure to insure them with the same company so you can get that sweet bundling discount.

- Military and veterans: Current service members and veterans receive insurance discounts almost across the board. If you're in this category, or you're the spouse or child of a service member or veteran, this should be one of the first things you tell your agent.

- Teachers: Carriers may offer teacher discounts to recognize their valuable work. You should always let your insurance agent know what you do for a living (so they can look out for other discounts), but it's extra-important if you're a teacher, since this is such a common discount. This discount may be offered through your union, so be sure to ask there.

- Union or professional association: Professional organizations often cut insurance discount deals for their members. Ask your rep or local leadership for details.

- Social, religious, and retirement organization: Just like professional organizations, social organizations cut insurance discount deals, too. Everyone from banks to advocacy groups like AARP offers discounts. Check websites and ask around the groups where you're a member.

- Loyalty: Love your insurance carrier? There are big benefits to sticking around. Loyalty discounts kick in after a certain number of years with a carrier.

- Referral: Love your insurance company, like a lot? Don't be shy about recommending them to friends and family. You might get a nice kickback discount.

Bonus round: high deductible discounts. If you agree to pay a higher deductible if you need to make a claim, your premiums will be lower. The insurance company will owe less, so they pass those savings on to you. Choosing a high deductible makes sense if you have enough savings on hand to cover minor home repairs on your own.

Save on Home Insurance

Our independent agents shop around to find you the best coverage.

How Hard Is It to Get Home Insurance Discounts?

The short answer: It mostly depends on the replacement cost of your home. Rambling Victorian mansions are charming, but they cost more to insure due to their complicated designs and older materials. A newer house with no turrets and up-to-date safety features will have cheaper premiums.

The hardest part of getting home insurance discounts is understanding when you're getting a discount. Some carriers will advertise their discount programs, while others just quietly factor savings into the final deal.

This is especially true with home insurance, where each insurance quote is based on a ton of different risk factors. Insurance formulas are always changing to reflect new risks. At the same time, your house may be aging and changing, too.

It's easiest to get insurance discounts if your home is newly built or renovated, but it's not the only way to get discounts.

Don't rule out renovation as a premium-busting option. Revamping a home can make it safer, slashing your insurance premiums while seriously raising its value. Sweat equity pays insurance dividends.

How Do I Get Home Insurance Discounts?

First, remember that you're probably already getting discounts based on stuff you don't have a lot of control over: your house's condition, location, and age. The savings might not be spelled out as discounts, but they're still discounts.

The next step is to do a little bargain hunting, both with an insurance agent and with your social network. Be sure to ask any major organization you're a part of if they offer discounts. That includes your union or other professional organization, bank, advocacy groups like AARP, and your place of worship, if you have one.

Remember, carriers can't take your religion into account, but your place of worship may organize discounts for its members, or encourage you to work with a certain company. For example, Thrivent Financial offers financial and insurance services primarily to Lutherans.

Working with independent insurance agents is another great way to get discounts. Independent agents aren't bound to one company's super-secret insurance formula. They can comparison shop between carriers and help you zero in on the best deal.

Here are the top factors that influence home insurance discounts:

- Fire risk: Low fire risk equals lower premiums. This comes down to the materials your home was built with, fire safety measures like sprinklers and fire extinguishers, and how fast firefighters can get to you.

- Crime risk: If you live in a low-crime area and/or install a security system, you and your stuff are safer. That's cheaper for the insurance company, so they lower your premiums.

- Location: Different states have different requirements for insurance, affecting premiums. On a granular level, different areas have different risks and varying access to emergency personnel like police and firefighters. All this affects your premiums.

- Natural disaster risk: The risk of earthquakes, tornados, wildfires, hurricanes, mudslides, floods, tsunamis, hail, windstorms, and avalanches all go into the big math soup that is your home insurance quote. Nowhere is totally safe, but some places (like California or the Gulf Coast) face more of these risks than others, driving insurance costs higher.

- Replacement cost: Remember, insurance isn't based on what you paid for your home. It's based on how much the insurance company could be on the hook for if you make a claim. The cheaper it is to replace, the cheaper your premiums will be. Here are two main factors to keep in mind when it comes to replacement costs:

- Unique or expensive materials: If the words "priceless" or "irreplaceable" come to mind when you think of countertops, floors, windows, and other neat features of your home, that probably means higher replacement costs--and higher premiums.

- Special features: Extras like saunas, pools, carriage houses, and ballrooms (if you're fancy like that) all raise replacement costs, and therefore your premiums. They can also raise the risk of injury. That's an anti-discount.

Home insurance discounts rest almost entirely on details about your home, unlike car insurance discounts, where your personal habits matter just as much as the make and model of your car.

Start by listing any valuable possessions you have in your home, such as fine jewelry, fur coats, precious metals, or priceless art. Home insurance helps protect your belongings, so what you store in your home can affect your premiums.

(You may choose to add something called a "floater" to your home insurance coverage, which is designed specifically to cover valuable items.)

Plus, there are a few personal details that do affect what discounts a carrier might offer you. Here's what your agent needs to know to find you the best deal:

- Your job, retirement status, and/or any US military association

- Marital status

- The size of your family

- Credit score

- Whether you're open to bundling additional insurance (car, life, etc.)

- What size deductible you're willing to accept (higher deductibles mean less coverage but lower premiums)

Once your insurance agent gets all the details about you and your property, they'll churn everything through the insurance formula. An independent agent will work with multiple companies so you can have a few different coverage options and rates to choose from.

Don't be shy about asking which discounts have already been applied to each quote and if there are more you could qualify for. Even if you're not eligible right now, it helps to know what you can expect down the line, too.

Planning to renovate? Don't forget to check in with your agent first. They'll have the inside scoop on things you can do to reduce home insurance costs, like picking out easy-to-replace materials or getting rid of fire risks.

Save on Home Insurance

Our independent agents shop around to find you the best coverage.

What's So Great about Independent Insurance Agents?

Now you know how discounts work. But we all know your time is valuable, so why sweat all the hard work yourself? Our independent insurance agents stay on top of the industry and all the latest discounts so you don’t have to. That means they’ll help find the right coverage, at the right price, for you.

They’re not just there at the beginning, either. If disaster strikes and you need to file a claim, they’ll be with you every step of the way, helping you meet deadlines and maximize your benefits. Besides, you deserve a cheer squad.